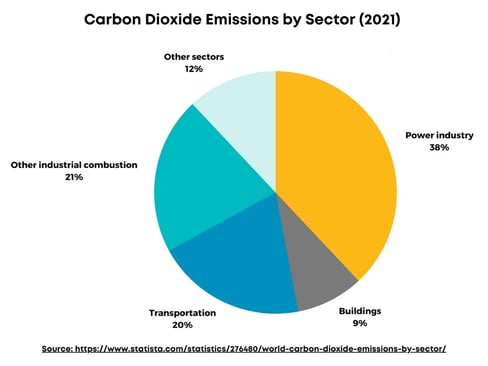

Who are the biggest CO2 emitters?

Carbon dioxide is emitted into the atmosphere by anthropogenic activities primarily consisting of energy production, transport, and industry. Electricity and transport emissions account for about 73% of the total GHG emissions globally, while about 5.2% of the CO2 emissions come directly from industry. Among industrial processes, cement production generates the biggest amount of carbon dioxide due to the direct release of this greenhouse gas during a chemical reaction. The iron and steel industry generates substantial CO2 due to its energy-intensive processes.

Other chemical and petrochemical processes are responsible in the industrial sector for releasing carbon dioxide, including ammonia production, which is used as a raw material in producing other materials such as cleaning products, plastic, fertilizers, pesticides, and textiles.

Upcoming regulations for CO2 emitters

In order to achieve the environmental goals set in the Paris Agreement, different authorities worldwide are setting new regulations. These regulations are based on the premise that each company can emit a defined amount of CO2 into the atmosphere; if the company exceeds the limit, it should pay a tax proportional to the amount of emissions exceeded.

For instance, in the European Union (EU), the EU Emissions Trading System (EU-ETS) allocated emission allowances for free to the manufacturing industries in the past, which has been gradually reduced. In 2013, around 80% of emission allowances were allocated for free; in 2020, only 30% were allocated for free. To encourage energy-efficient industries, free allowances are allocated according to benchmarks; installations that do not meet the efficiency benchmark will need to reduce their emissions and/or buy additional allowances to cover their emissions.

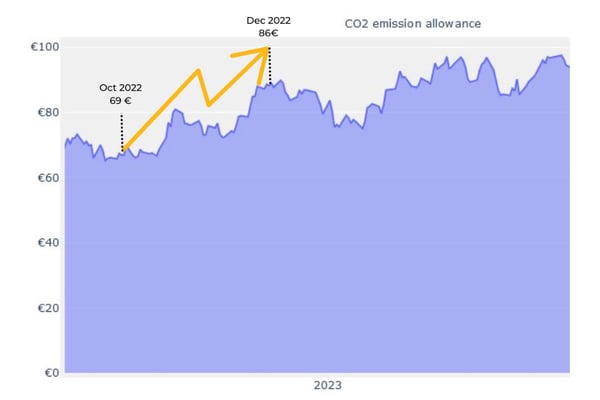

The EU-ETS is based on a cap-and-trade model where companies can buy or receive emission allowances (1 Allowance = 1 ton of CO2 emitted) with others that need them if they have allowances remaining. The trading system is set to be a fair and transparent process through auctioning the allowances; since the cap is reduced yearly (to reduce total emissions), the price of allowances rises with time. For instance, during October 2022, the average auction clearing price was €69.19/allowance; for December 2022, the price rose to €86.76/allowance.

Source: https://sandbag.be/carbon-price-viewer/

In the upcoming years, from 2026 to 2030, the EU-ETS is eliminating the free allocation of emission allowances to ensure emissions reduction and achieve the goal set for 2050 of carbon neutrality. According to analysts, EU allowances are expected to average €86/ton of CO2 in 2023 and €96/ton of CO2 in 2024, while the forecast for 2025 is about €105/ton of CO2. Considering this forecast for the CO2 price, for example, an average factory of bulk chemicals receiving around 55000 free allowances (with an estimated cost of 4,730,000€), in 2026, when the free allocation is eliminated, such a chemical factory would expect to pay about 5,775,000 €.

The impact of the CO2 price on the industry is expected to increase, hitting the profit margins of manufacturing companies. For instance, for an average cement factory, the impact on the production cost at €55/ton of CO2 accounted for about 8-10% of the total cost (the price of CO2 in 2022), with the increased price to €90/ton, the cost of carbon dioxide accounts for about 12-15% of the total cost. This estimate was made by the European Cement Association by the end of 2021. Therefore, companies are encouraged to search for alternatives to reduce the economic impact of environmental regulations, which will have a greater impact in the next few years (2026-2030).

What can companies do to reduce their emissions?

Many industries seek the most energy-efficient processes to avoid or reduce taxes due to GHG emissions. However, this may not be enough, and alternative strategies are required, especially for energy-intensive processes. Implementing appropriate carbon capture, utilization, and storage (CCUS) technologies can help companies achieve emission reduction and energy-efficient processes.

The early implementation of carbon capture and storage strategies can be the difference on the road to reducing emissions and cost advantages associated with emissions as well as a competitive advantage in terms of social reputation/recognition. For instance, in the cement industry, integrating appropriate carbon capture could reduce emissions by up to 36% with minor modifications to the production process.

Different decarbonization options exist in pre- and post-combustion steps, including oxyfuel combustion, amine scrubbing, calcium looping, and adsorption technologies. The major concern of companies for implementing carbon capture and storage technologies is the high energy consumption associated with the carbon capture step.

Among the carbon capture technologies, amine scrubbing is the most mature option but is energy intensive. In this method, liquid amines are put into contact with flue gases inside a reactor where CO2 is transferred to the liquid. After absorption, carbon dioxide is released from the amine solvent in a steam reactor with a higher temperature between 120–150 °C. The CO2 solubility decreases at higher temperatures, allowing solvent regeneration for a new capture cycle.

Alternative technologies for carbon capture include adsorption with solid sorbents. Advanced physisorbents such as MOFs that selectively capture CO2 from flue gas streams offer the most significant upside potential for a revolution in carbon capture technology since they would require much less energy for regeneration (regeneration temperatures below 90 °C) and exhibit high working capacity. Compared to other adsorbents, MOFs offer uptake capacity, selectivity, humidity resistance, and low-energy requirements advantages.

Therefore, implementing adsorption-based technologies using MOFs can support reducing carbon dioxide emissions in an energy-efficient process. Combined with adequate technologies for each industry, this could reduce the impact of taxation implemented by environmental protection authorities.

Please visit our previous blogs and success stories to learn more about MOFs.

.jpg)